Home » Global Logistics Market Update

Freight rates jump on early peak season, frontloading; DOJ moves to appeal IEEPA refunds; Sec 232 tariff adjustments

Roughly three months into the Middle East crisis, the situation remains highly volatile and unpredictable, with talks now reportedly called off by Iran, alongside a threat to completely close the Strait of Hormuz due to an increase in US and Israeli attacks. The Trump administration, however, has called this claim untrue, saying that talks are ongoing, but that the deal is “not a simple thing.” This pattern is what we’ve seen throughout the war, with Iranian and US media often contradicting reports from the other.

The Strait of Hormuz has remained closed, with continued vessel incidents this week alongside reports of a suspected Iranian mine spotted in Omani waters, reinforcing the safety risks to shipping in the region. For shipping, the overall situation has not changed much; the blockade continues to sustain pressure on bunker availability and fuel costs, creating higher operating costs, ultimately being passed down to customers. Global VLSFO prices have trended downward over the last two weeks, with a slight uptick after the recent report of Iran backing out of talks, but remain elevated with the crisis ongoing.

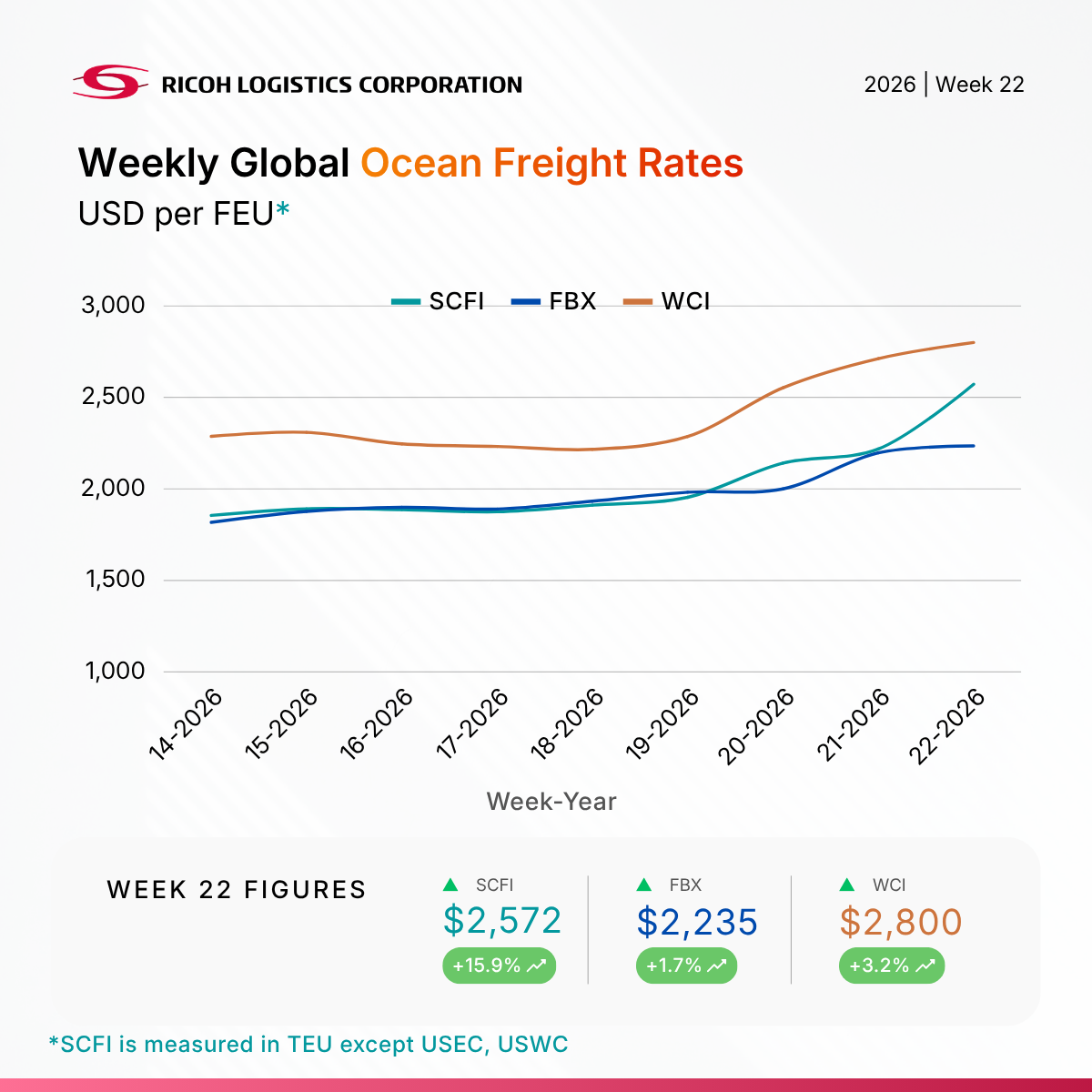

Global container rates increased across major freight indices again this week, with the most significant gains in the SCFI, which jumped 15.9% to $2,572. Drewry’s WCI rose for the fourth consecutive week, up 3.2% to $2,800/FEU, and Freightos FBX rose 1.7% to $2,235/FEU. These global gains were primarily driven by higher rates on transpacific and Asia-Europe, Mediterranean lanes.

Primary factors pushing up transpacific and Asia-Europe rates are an early arrival of peak season demand along with shipments being frontloaded ahead of an expected July 1 bunker fuel adjustment. Rates are expected to increase further in coming weeks across these lanes as peak season approaches and carriers continue to push for rate increases through FAK and PSS adjustments alongside capacity management.

Freightos reported daily rates on transpacific, Asia-Europe, and Mediterranean trades have seen additional $1,000-$1,800/FEU jumps so far this week on June 1 GRI and PSS introductions, including a $2,000/FEU PSS announced by ONE on transpacific eastbound cargo. Additional FAK, PSS increases are planned for mid-month on the lanes as well.

On the transpacific, eight blank sailings have been announced for this week, indicating tighter capacity, while Asia-Europe appears relatively stable with only four blank sailings announced, according to data from Drewry’s Container Capacity Insight. Over the next five weeks, 47 out of 707 departures are expected to be cancelled, which represents a 7% cancellation rate. The most heavily impacted is transpacific eastbound trade, making up 49% of service disruption, followed by Asia-Europe/Mediterranean at 34%.

The US Department of Justice (DOJ) requested to pause IEEPA tariff refunds in a court filing, signaling intent to appeal the federal court order that mandated universal IEEPA tariff refunds. The DOJ has a 60-day period ending June 6, 2026 to file an appeal after the original case was reissued on April 7.

“The defendants intend to appeal the Court’s universal injunction and to seek a stay of the injunction except as to the particular importer plaintiffs in each case in which the Court has entered the injunction.”

This came in response to a May 27 show cause order by Judge Eaton, requiring a Customs and Border Protection (CBP) Commissioner to appear before the court on June 9 to answer question on tariff refund implementation and why the suspension order should remain in place.

In the response filing on May 29, the DOJ challenges both the requirement for the Commissioner to appear in court as well as CBP’s authority to issue refunds for entries that have completed the liquidation process without a court order involving that specific importer. “CBP has no authority to reliquidate or refund money without a court order,” the DOJ argued.

Later the same day, Judge Eaton denied the DOJ request, leaving in place both the order to appear before court and the universal injunction requiring CBP to reliquidate all entries subject to IEEPA duties, including fully liquidated money.

Prior to this appeal announcement, CBP launched the Consolidated Administration and Processing of Entries (CAPE) portal in April to manage the $166 billion in available refunds. According to a CBP court filing on May 26, the portal has accepted $85 billion in potential and certified refunds. As of May 22, $20.6 billion of that total had been transferred to the US Treasury Department for disbursement.

The appeal introduces potential disbursement delays for the 330,000 US importers eligible for restitution following the Supreme Court’s February decision striking down the tariffs. If the universal order is overturned, legal experts indicate the court would need to approve refund eligibility on a case-by-case basis. President Trump previously stated shortly after the Supreme Court decision that litigating these refunds would take years.

Section 232 adjustments: President Trump announced in a proclamation that the administration is temporarily adjusting Section 232 tariffs on metal-based industrial and agricultural equipment from June 8 until the end of 2027.

These changes reduce the duty from 25% to 15% for agricultural machinery like combines and residential HVAC systems, while also extending the 15% rate to mobile industrial equipment such as forklifts from specific trade-deal partners. A preferential 10% duty rate is available for capital equipment containing at least 85% US melted and poured steel or smelted and cast aluminum by weight

For imports from Canada and Mexico, the 25% duty applies only to the non-US content of the product, provided the total effective duty remains at least 15%. Other partners including the EU, UK, Japan, and South Korea will see a total effective duty of 15% (if the standard duty is below 15%) or 0% additional Section 232 duty (if the standard duty is already 15% or higher).

Section 301 forced labor proposal: The Office of the US Trade Representative (USTR) has announced a proposal for a 10-12.5% tariff under Section 301 to address forced labor, with 60 countries identified as trading in goods produced through such practices.

Under this plan, economies that have already established prohibitions, entered reciprocal trade agreements, or created partial regimes to prevent forced labor trade would face a 10% additional duty, while all other investigated economies would be subject to a 12.5% tariff. The proposal includes a textile mechanism allowing for reduced rates on specific volumes of apparel and textile imports from certain countries, though products listed in Annex A of the Federal Register notice are exempt.

The USTR will hold a public hearing on July 7, with written comments due by July 6.

Section 301 proposal on Brazilian goods: The USTR has proposed a 25% Section 301 tariff on various Brazilian products following an investigation into the country’s practices regarding digital trade, intellectual property, illegal deforestation, and ethanol market access.

This proposed action allows for several exemptions, including goods already covered by Section 232 tariffs, raw materials that are unavailable domestically, and products that might cause widespread economic disruption or cannot be produced in sufficient quantities in the US.

A hearing regarding these Brazilian trade sanctions is scheduled for July 6, 2026, and the deadline for submitting written comments is July 1.