Home » Weekly Logistics Update

Hormuz tension continues as freight rates bump up; Section 122 tariffs ruled illegal; International Roadcheck begins

Just two days after launch, the US suspended “Project Freedom,” an operation to escort ships out of the Strait of Hormuz that triggered a fresh wave of regional hostilities. At the same time, Iran launched a formal Persian Gulf Authority, which will grant transit permission and potentially collect tolls in exchange for passage through the waterway.

The ceasefire remains in effect, but tensions are high and both sides remain far apart in reaching an agreement, with each rejecting a proposal from the other this week. The US Naval blockade is still in place, with the US Central Command (CENTCOM) reporting 65 commercial vessels have been turned away and 4 disabled.

Dark vessel transits have surged according to TradeWinds. The data provider reported a 600% surge in vessels transiting without AIS signals between April 19 and May 3. The report said that while AIS data showed little activity, overhead surveillance for the same time period revealed both containership and tanker movements near Larak Island, Kharg Island, Bandar Abbas, and Fujairah. Further deteriorating vessel visibility is electronic interference, with roughly 470 ships being affected by GPS jamming over a 24-hour period near Fujairah and Khor Fakkan.

Disruption to vessel schedules continue due to congestion, delays and rerouting. Industry sources say alternative Gulf ports have began gradually reopening gates to outbound freight, which may take some pressure off terminal yards and improve equipment circulation.

Fuel availability across key Asian hubs remains tight, with bunker refueling wait times reaching up to 15 days at Singapore and Japanese ports. S&P Global analyst Fotios Katsoulas warns this lead time could become a “global standard” for refueling if the Strait of Hormuz stays closed for another month.

Maersk said last week that its monthly fuel expenditures have doubled to $500 million since the regional conflict began, an expense they confirm is being passed on to customers “in full.” CEO Vincent Clerc said in a press conference that even with a resolution, the energy crisis is expected to last “at minimum several more months, possibly many more months,” citing conversation with oil companies.

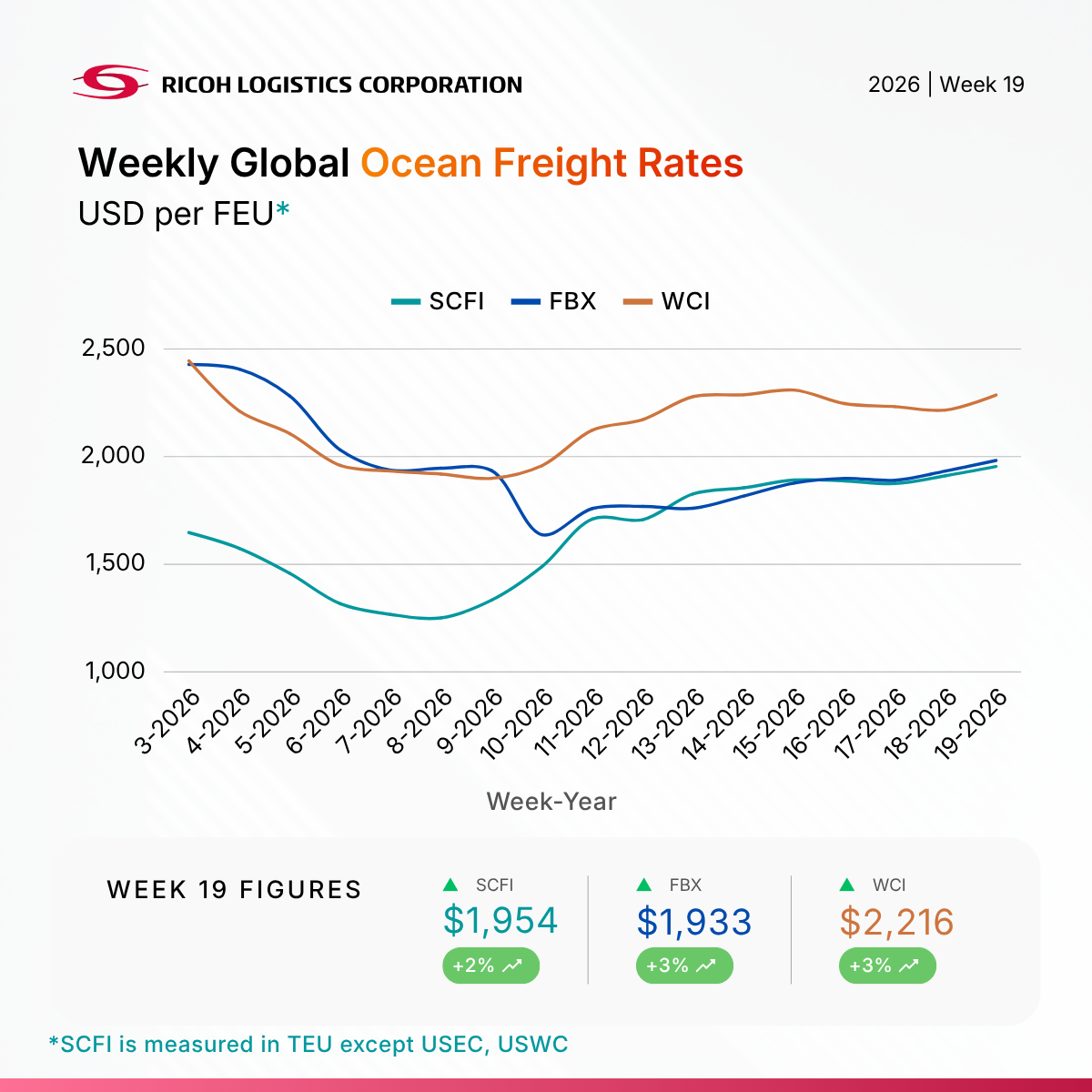

Drewry’s WCI increased 3%, ending three consecutive weeks of decline. Transpacific rates rose, up 7% from Shanghai to New York and 5% to Los Angeles as carriers implemented Emergency Fuel Surcharges (EFS) and Peak Season Surcharges (PSS). Space is expected to tighten in the coming weeks. Shanghai to Rotterdam rates were up 2% and those to Genoa edged up by 1%. Carriers continue to manage excess capacity with blank sailings and capacity reductions. CMA CGM, Hapag-Lloyd and MSC have announced FAK rate increases that take effect Friday, though the current supply-demand dynamic makes successful implementation unlikely.

Looking ahead, the US peak shipping season may be muted this year, the National Retail Federation suggested in its latest Global Port Tracker report, with rising inflation, falling consumer confidence, and stalled restocking efforts lowering import volumes. The NRF anticipates a nearly 8% year-over-year decline of 2.2 million TEUs in July, with volumes progressively weakening into August and September, down 5.5% and 1.3% year-over-year respectively.

Air cargo capacity in the Middle East continues to gradually recover, according to DHL Global Forwarding (DGF). “Overall, we have noticed a further increase in air freight capacity being available and a first softening of rate levels, but they are still at significantly elevated levels versus pre-crisis,” Tobias Maier, DGF’s CEO for the Middle East and Africa, said in a webinar. “We are also seeing the first sign of airline fuel surcharges starting to come down, with reports emerging that airlines are prioritizing international flights over domestic ones.”

Global air cargo rates are up 30% since the start of the crisis and year-over-year, prompting some Asia-Europe shippers to shift to sea-air services via the US West Coast to cut costs. While rates have eased from their peak in mid-April, they are expected to remain elevated for some time. “Given the current state of disruption to jet fuel supplies, it seems unlikely rates will fall back sharply any time soon” TAC Index noted in an update published Friday.

In another legal blow to the Trump administration, the US Court of International Trade (CIT) ruled that the 10% global tariffs imposed in February were illegal, finding that the administration failed to properly justify the tariffs under Section 122 of the 1974 Trade Act, which allows a president to impose tariffs up to 15% to address “large and serious United States balance-of-payments deficits” without approval from Congress.

Per the ruling, the administration must cease collecting these tariffs from the plaintiffs and refund prior payments plus interest within 5 days. For now, this outcome applies only to the specific plaintiffs in the case. The 10% tariff will remain in effect for all other importers until it expires in July. Nevertheless, a second ruling of this kind highlights the instability of the administration’s tariff regime, following the earlier ruling that struck down IEEPA tariffs.

In response, President Trump said his administration would “do it a different way” – the same defense he used after the IEEPA ruling that resulted in these now-challenged global tariffs. On May 8, the administration filed an appeal against the court’s ruling.

In a May 1 Truth Social post, President Trump threatened to impose a 25% tariff on EU trucks and cars, up from the baseline 15%, saying the EU is not moving quickly enough to reduce tariffs on US goods.

EU negotiators met last week to discuss the US deal, but failed to reach a conclusion. Talks are scheduled to resume May 19.

The President initially said the EU could face the higher tariffs “starting next week” from the original post, but has now set a July 4 deadline for the trade agreement to be ratified.

Ursula von der Leyen, President of the European Commission, posted on X last week that the EU remains “fully committed” to implementing the deal. “Good progress is being made towards tariff reduction by early July.”

The Commerce Department published a Federal Register notice yesterday outlining the procedures to apply for Section 232 tariff reductions for pharmaceutical products. Applications must be submitted to pharma232@bis.doc.gov within 30 days from the publication date (May 11).

The annual Commercial Vehicle Safety Alliance (CVSA) International Roadcheck is taking place this week, starting today, May 12 through Thursday May 14. Over this 72-hour period, CVSA inspectors conduct high-volume roadside safety inspections of both commercial vehicles and drivers across the US, Canada, and Mexico to ensure compliance with federal and state regulations.

According to the CVSA, nearly 15 trucks and motorcoaches are inspected every minute over the three-day period. Most vehicles undergo the 37-step Level I inspection, but some will receive a Level II, III, or V inspection. Each year’s inspection efforts designate a special area of focus for both vehicles and drivers. The focus areas for 2026 are cargo securement for vehicles and ELD (electronic logging device) tampering for drivers.

Domestic trucking capacity is expected to tighten during the event as some carriers suspend operations to avoid heightened inspection scrutiny and potential out-of-service (OOS) orders. Larger carriers may be more motivated to avoid potential violations as their scale makes them more susceptible to litigation if found non-compliant.

Spot rates may also see a bump during the week. Last year, Freightwaves SONAR recorded a 7% increase in dry van spot rates, an 9% increase in reefer rates, and a 7.5% increase for flatbed during the International Roadcheck. However, due to the timing, it is difficult to separate the Roadcheck’s impact from Memorial Day’s due to the timing.

Of the 56,178 inspections conducted during the 2025 Roadcheck, there was a 18.1% vehicle OOS rate and a 5.9% driver OOS rate. This means that until the violations were resolved, the drivers and/or vehicles were restricted from further travel. The top violation category for vehicles was brake systems (24.4%), followed by tires (21.4%). The top violation for drivers was hours of service (32.4%), followed by no CDL (24.4%).