Home » Weekly Logistics Update

Transpac, Asia-Europe rates surge, Panama Canal worries grow as El Nino looms, SCOTUS case sets new liability reality for the industry

US-Iran talks have not progressed and the Strait of Hormuz remains tightly controlled, drawing threats from President Trump that “time is ticking.” The President said yesterday on Truth Social that the US is holding off on a strike on Iran planned for today to allow for negotiations to continue.

The physical security situation for unapproved or non-cooperating vessels remains volatile. The UK Maritime Trade Operations (UKMTO) reported a Chinese vessel anchored 38 nautical miles northeast of Fujairah in the UAE was seized on May 14. Another vessel, an Indian-flagged cargo ship, sank off the coast of Oman following an attack on May 13 that led to a fire on board. All crew members were rescued.

On the US side, CENTCOM reports 78 ships have been turned around and 4 disabled by the US blockade as of May 16. The US operation appears to be partially successful, with some Iranian-linked movements blocked and some making it through to Iranian ports.

Traffic in the Strait of Hormuz is still constrained. There has been a small, steady flow of transits moving through Iran’s designated route. Most movements are outbound, likely due to carriers looking to retrieve their vessels for use elsewhere.

Global average bunker prices (VLSFO) steadily trended up over the past week, but still sit about 9% below the early April peak. The May edition of the IEA’s Oil Market Report expects that ongoing supply disruptions in the Strait of Hormuz will keep the broader oil market in a deficit through late 2026. Further bunker price volatility is expected heading into peak summer shipping season.

The highly anticipated Trump-Xi summit in Beijing concluded last week, establishing a stabilizing framework for ongoing negotiations and a joint agreement of “constructive strategic stability,” suggesting tensions may have eased to some degree. China said this framework will set the tone for at least the remaining three years of Trump’s time in office. The two nations agreed to set up a new “Board of Trade” to manage bilateral trade across non-sensitive goods.

In the meantime, China committed to resuming some purchases of US agricultural products, energy, and Boeing aircraft, with four US LNG tankers already en route to China. Both leaders also agreed the Strait of Hormuz must remain open to commercial transit, though it remains to be seen how actively China will intervene to stabilize the region.

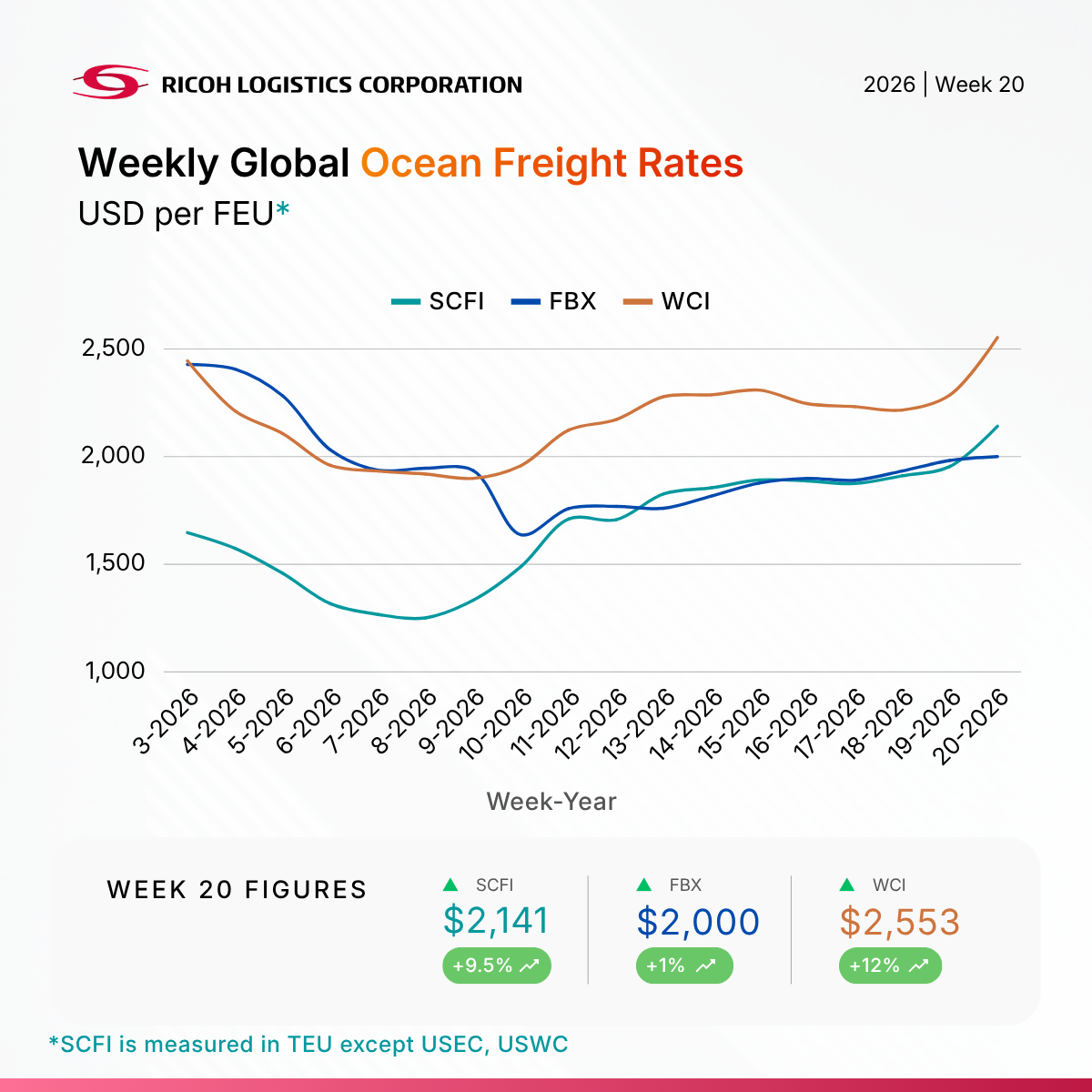

Global ocean rates jumped this week on the SCFI and Drewry WCI – up 9.5% and 11.7% respectively, while the FBX saw a mild bump of 0.9%. These sharp gains are largely driven by a combination of carrier pricing strategies, disruption, and elevated operational costs on Transpacific and Asia-Europe trade lanes.

Transpacific rates increased 14% from Shanghai to New York and 10% to Los Angeles on the WCI, as carriers implemented Emergency Fuel Surcharges (EFS) and Peak Season Surcharges (PSS), with capacity operating at 78% of usual levels this week. Carriers continue to steadily manage capacity with 7 blank sailings announced on this lane for the next week. Rates are expected to rise further next week.

Asia-Europe rates on the WCI rates jumped 20% from Shanghai to Genoa and 11% to Rotterdam. Though the status quo has been weak demand and oversupply, peak season is expected to start earlier than usual because of longer transit times. Blank sailings will cut roughly 12% of capacity through late May, while demand may see a rebound with peak season approaching and push rates up further. Carriers are planning further rate increases from June 1, aiming to push rates up roughly $2,000/FEU from current levels.

On the SCFI, rates from Shanghai to South America saw massive gains, up 29% to the East Coast and 25% to the West Coast. In addition, the Shanghai-Dubai rate surpassed $4000/TEU, 350% higher than pre-crisis levels.

Middle East air cargo traffic continues to operate under a dynamic of limited capacity and elevated costs. Freightos Air Index recorded a divergence across different trade lanes. China, South Asia and SEA to Europe rates continue to follow past observations of being elevated relative to pre-crisis levels, but remaining flat/beyond peak levels week over week. SEA – Middle East rate in contrast reached a new peak of $4.75/kg and continue to climb up this week according to Judah Levine, head researcher of Freightos, while S. Asia – ME prices have also climbed over $4.00/kg.

Regulatory changes in the EU are likely to dampen e-commerce air volumes into the region. France implemented the EU-wide €2 per item tax on small parcels early, and has seen a steep drop off in parcel volumes as cargo was diverted to nearby countries and brought into France by truck. Vatry Airport saw a 65% drop in air cargo volumes over ten weeks, along with a 92% fall in customs declarations at Paris CDG. The broader EU-wide tax is set to take effect in July.

Congestion is building at the Panama Canal ahead of scheduled maintenance on the Gatun Locks’ east lane from June 9 to 17. During maintenance, daily transit slots will be cut to 16.

Wait times are already hovering around 47.9 hours (up 60% from January-February, before the start of the Hormuz crisis), Scandinavian investment bank SEB says. The upcoming transit slot cuts may worsen delays, forcing vessels to reroute or experience extended wait times.

Along with the scheduled maintenance, weather risks are growing. The US National Oceanic and Atmospheric Administration estimates an 82% chance of El Niño developing between May and July.

“El Niño is likely to emerge soon (82% chance in May-July 2026) and continue through Northern Hemisphere winter 2026-27 (96% chance in December 2026-February 2027). While confidence in the occurrence of El Niño has increased since last month, there is still substantial uncertainty in the peak strength of El Niño, with no strength categorization exceeding a 37% chance.”

El Niño has historically led to drought and suppressed rainfall in Central America, drying up the Gatun Lake and lowering the canal’s water levels. When this happens, the Panama Canal Authority implements draft restrictions and may also reduce daily transit slots. Draft limits reduce available capacity as carriers must reduce volume to meet restrictions, while transit cuts can lead to congestion and delays.

It is also worth noting the timing of these events coincides with the traditional peak season, though retail forecasts have indicated that this year’s volumes may be muted compared to previous years.

Despite these growing concerns, the Panama Canal Authority has downplayed the risk, maintaining that there are no plans to reduce vessel traffic through the rest of the year. Officials say that water conservation measures have kept water levels in the Gatun Lake high, and despite rising demand, the canal is handling roughly 38 vessels per day.

Freight brokers can now be sued for negligent hiring, the Supreme Court ruled 9-0 on Thursday in Montgomery vs Caribe Transport II. The unanimous decision clarified that FAAAA preemption does not shield brokers from safety claims. In this case, Montgomery sued C.H. Robinson for severe injuries suffered from an accident involving the truck the broker had arranged.

While this case explicitly centers on a broker, the implications are significant for the industry as a whole. The liability also applies to 3PLs, forwarders, digital booking platforms – any party involved in carrier selection. Shippers who may have assumed a broker’s preemptive defense would in turn insulate the transaction from liability can also no longer do so.

Although we can’t be entirely certain about the full impact until it actually plays out, we may be looking at the start of a significant change in the industry into a more rigid, safety-first model.

To ease some of the fears from this ruling, Justice Kavanaugh stated that proving ordinary care in carrier selection remains a viable defense. This means brokers will not be automatically held liable – they must however have evidence to show they are taking reasonable care to evaluate each carrier for safety.

The financial implications of this ruling are significant. Unlike the strict federal insurance minimums placed on carriers, freight brokers are only required to hold a $75,000 surety bond, which handles financial responsibilities to shippers and carriers – not liability. With the federal shield removed, we now know brokers are fully exposed to jury awards that can easily scale into eight, nine-figures. This added liability will be reflected in higher insurance premiums and stricter underwriting requirements.

Thus, carrier vetting and documentation of that process will become much more crucial both for legal defense and securing insurance. This can include public data (FMCSA’s SAFER system, crash and OOS rates, inspection history), internal records, a documented vetting processes, and the shipper’s records and criteria.

While no one has a crystal ball, the plausible outcome is that trucking is going to feel some growing pains as the industry moves towards prioritizing safety. We could see a progressive tightening of usable capacity as brokers phase in stricter compliance filters. Smaller operators may also increasingly consolidate under larger carrier networks to utilize their corporate compliance infrastructure, introducing higher operational cost floors to the spot market.

And with the state of global freight rates amid geopolitical uncertainty and tariffs, cost-cutting anywhere possible is enticing. However, brokers and shippers who chase the cheapest capacity without strict safety vetting are now taking a huge risk.